[av_textblock size=” av-medium-font-size=” av-small-font-size=” av-mini-font-size=” font_color=” color=” id=” custom_class=” av_uid=’av-ke2tekhd’ admin_preview_bg=”]

Covid-19 and the impact on Southern European tourism: Portugal as a case study

[/av_textblock]

[av_image src=’https://www.allaboutretirementoverseas.com/wp-content/uploads/2020/05/Covid-19-S-Europe-photo-300×123.png’ attachment=’3591′ attachment_size=’medium’ copyright=” caption=” styling=” align=’center’ font_size=” overlay_opacity=’0.4′ overlay_color=’#000000′ overlay_text_color=’#ffffff’ animation=’no-animation’ hover=” appearance=” link=” target=” id=” custom_class=” av_element_hidden_in_editor=’0′ av_uid=’av-ke2tahkn’ admin_preview_bg=”][/av_image]

[av_textblock size=” av-medium-font-size=” av-small-font-size=” av-mini-font-size=” font_color=” color=” id=” custom_class=” av_uid=’av-ke2tb218′ admin_preview_bg=”]

The tourism industry was the first sector to be affected by the measures implemented as a result of the Coronavirus pandemic. The effects were immediate and dramatic. The EU’s commission for economy declared on May 5th that the bloc had entered the deepest economic recession in its history. Southern European countries are particularly susceptible to the suspension of flights, closure of hotels and restaurants and, most importantly, the lock-down of people that prevented them from travelling anywhere.

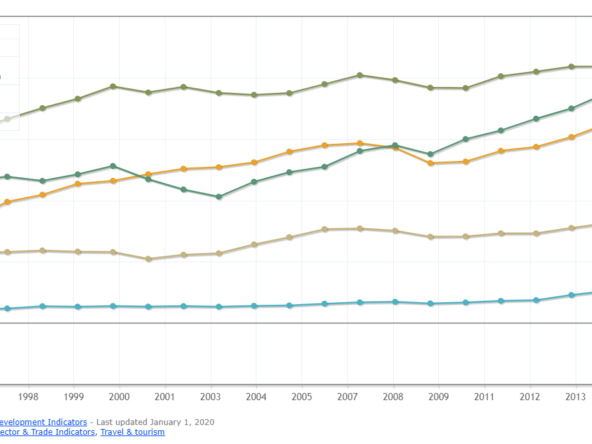

Tourism, travel and related services represent 10.3% of global GDP, 10.1% of European GDP, 15% of Spanish GDP and 17% of Portuguese GDP*. Foreign tourism alone represents 8.7% (and over 18% of exports). * approximate, may vary due to different sources.

Portugal’s economy is expected to contract by 6.8% in 2020. Spain’s by 9.5% and the EU as a whole by 7.4%. Interestingly, it is one of the few times, after a crisis, that I can recall a Portuguese financial or economic metric being better than the European average. And according to the infographic, of the “Big 5” Southern European tourism destinations, Portugal appears to be the market expected to suffer the smallest impact.

Unemployment, despite dramatic measures put in place by governments will increase, in some countries such as Greece and Spain, to levels of 19.9% and 18.9%, respectively. Questions are being asked about how government will fund unexpected emergency programmes and debt levels are expected to rise dramatically, in Portugal’s case from current levels of around 117% to 131% of GDP. In the UK, the question is what mechanism will be used to fund the £8 billion injection into the economy, mainly the furlough programme, that saw the UK government paying the salaries of around a third of all working adults.

The severe impact of the pandemic on Europe’s economy is being reported globally. One of the first reports I found was from a newspaper in Pakistan!

In Greece, the Hellenic Chamber of Hotels found that 65% of hoteliers said they were likely to go bankrupt. In early April, reports were that 74% of companies in Portugal linked to tourism, were closed. The encouraging news is that the majority of these companies did not lay off staff, even though 70% of companies expected zero turnover for May. By May, reports were that 80% of hotels and tourist accommodation had suffered cancellations in the period of March to August. The Centre and Lisbon regions of the country saw the greatest falls in bookings, with the Algarve remaining the most popular choice for visitors.

A news article in early May indicated that average earnings of Portuguese workers had fallen by 5.3%. Not only does this seem remarkably little, considering that many businesses in the tourism industry registered little or no turnover, but it emphasises how much the tourism industry has suffered relative to the economy as a whole. Estimates are that European economies will “rebound” by 6.1% in 2021.

The speed at which economies will start to recover is linked to the pace at which individual governments release countries from lock-down, reduce restrictions such as the banning of flights or limiting foreign visitors, and also manage any second wave of infections. As we have predicted, this was never likely to be before mid-June and the European Commission has now requested that the European Parliament extend the non-essential travel ban to the middle of that month.

Both outbound and inbound markets must agree, for tourism flow to restart

A certain tension exists between the wish to start travelling again, and a fear of whether destinations will be safe. According to DutchNews.nl, for “tourists wanting to head south much will depend on the government policies of popular holiday destinations such as Spain, Italy and Portugal.” Others prefer to stay at home. The publication reports that 7.2 million people prefer to staycation rather than risk overseas travel in 2020.

However, a survey of 2,000 American travellers by the Overseas Leisure Group shows that of the 72% of travellers planning their next holiday, 78.2% are prepared to fly and more than 50% want to travel by the Fall/autumn. 67% of travellers questioned had a daily budget of $500 or more. 26.1%, the largest group, stated that they would opt for a trendy beach destination. A separate survey by Aggressor Adventures stated that 66% of respondents (admittedly a small sample) wanted a water holiday. So it seems that perhaps the North American market, despite still representing a small portion of inbound traffic to Europe when compared to European visitors, may shine a ray of hope on an otherwise rather dour landscape.

There is no better example of the tension described above than the airline industry. In the UK market, Wizz Air and EasyJet have defined travel dates as early as May and June, respectively. But it is their choice of destinations that provides us with some insight into the perception of risk. Wizz Air started flights to Tenerife and Lisbon on May 1st. EasyJet started flights to Spain on May 1st, for essential travel. It would appear that both airlines want to position themselves as leading the kick-start of the industry, in particular via the implementation of safety measures such as social distancing, that larger rivals such as Ryanair have said are impractical, and use of face masks.

EasyJet will re restarting flights to the Algarve in June, in line with the company’s policy to go ahead with EasyJet Holiday bookings in June, July and August. EasyJet’s Portugal Director defends the decision by stating that the airline expects 75% of the country’s hotels to have reopened by that time. Local industry is emphasising Portugal’s safety record, in particular its success in managing the Coronavirus pandemic. Elidérico Viegas, president of the Algarve hotelier association, was quoted as saying that “Portuguese and foreign holidaymakers, particularly British, are looking to us [Algarve] as a Covid-safe destination.”

It is only a question of time until the more aggressive tourism associations start to use direct comparisons between countries with good and poor coronavirus responses, to market their destinations. An astute marketing campaign might highlight that it might actually be safer for tourists to travel to a safe foreign destination, such as Portugal, than to staycation in a dangerous home country with a poor Covid-19 response, such as the UK or the US.

The UK’s mismanagement of the Coronavirus pandemic

The UK failed, and is failing, in its coronavirus management, and specifically its testing policy. I have explained the link between government inaction and rhetoric, and medical outcomes, in an article www.allaboutretirementoverseas.com/2020/05/06/government-and-covid-19/. At time of writing, UK opposition politicians have criticised the Prime Minister’s new message to the nation as vague and confused. Scotland’s First Minister has decided not to change the message north of the border.

The decision, on March 12th, by the UK government to stop testing outside hospitals, the exclusion of key workers from access to testing, and the omission of the social care sector, both residents and carers, from both testing and statistics, have now been confirmed as key reasons why the UK has Europe’s highest death toll, and also why it has not yet managed to define a lock-down exit plan. Reuters questions whether the UK’s Prime Minister, Boris Johnson, is a “lovable rogue or dangerously incompetent.” The Independent is more direct in stating that “Johnson’s mistakes have led to thousands of deaths.”

The UK’s attempt at a tracking app is in a shambles, having stumbled at the first hurdle, and the country’s Prime Minister has, inexplicably and to the surprise of even his health secretary, doubled the testing target to 200,000 a day when the country has consistently failed to reach its first target of 100,000. In addition, testing levels have now fallen to below 70,000 due to a shortage of chemicals required in the testing process, and tests are being flow to the US for analysis. If it were not so tragic, the situation would not be out of place in a Monty Python sketch.

This at a time when most countries that have seen their infection curves pass their peak, are advocating a move to antibody testing. I am not alone in criticising Johnson’s absolute lack of grasp of the detail and his failure to fully explain, during his first Prime Minister’s Question Time, why the government felt the need to announce the easing of lock-down restrictions (unknown and undefined at the time) on television rather than to Parliament. However, it is clear why he has adopted the approach. In line with the increased acceptance, by the UK public, of fake news and fuzzy answers, Johnson understands that his likely fudged plan will have a much greater chance of acceptance by a television audience than via a parliamentary debate.

Internationally, the UK is now starting to attract substantial and widespread criticism for its mismanagement of the Covid-19 pandemic. This despite the country having undertaken a full dry run for a mass outbreak of killer flu, known as Exercise Cygnus, several years ago. The government refused to release the results in 2016 despite requests from opposition parties to do so, and clearly did not use the recommendations and findings of that exercise to prepare for the Covid-19 response. As reported by inews, descriptions of the UK’s handling of the pandemic range from “a shambles”, “a nightmare” reflecting “negligence”, “complacency” to “stupidity”.

The Sydney Morning Herald in Australia highlights the UK’s response as “the biggest failure in a generation”. Germany’s Focus describes “how Britain became Europe’s problem child”. Boris Johnson’s delayed announcement of a lock-down on March 23, weeks after bragging openly about shaking hands with patients on a coronavirus ward on March 3rd, and also after the decision on March 12 to stop testing people at home, has rightly been criticised at home and abroad. The Prime Minister decided that allowing large sporting events such as the Cheltenham Festival, with 250,000 attendees, in March, was acceptable in terms of the risk of infection.

Attributing an attitude of “superiority” to the way in which Britain did not deal with the pandemic, the New Yorker’s description perfectly describes Johnson’s initial view that to declare a lock-down was somehow to remove the inalienable right of the British nation to its freedom. The Prime Minister’s bumbling approach has cost lives and irrevocably affected the health of many more people. While his medical team quickly identified the need for Johnson to be hospitalised, many did not have the benefit of the same preferential treatment. Without testing, the solution for millions was the only one recommended by the government: self-management in self-isolation.

I am an example of someone infected during exactly the period in question, and a victim of the Prime Minister’s frankly reckless behaviour. Without doubt if I had access to testing, the accompaniment I would have received would have been much more intense and the seriousness of my symptoms, which were severe, would have resulted in earlier diagnostics. Compare this abandonment of the patient to a story told to me by a Portuguese reporter, whose family had all suffered mild symptoms but had been accompanied by a doctor and two nurses, each one checking up on whether the other one had identified any and all symptoms and possible causes.

The fact that the UK appears to be spectacularly unable to get ahead of events in terms of the management of the Covid-19 pandemic, means that its actions are having unintended consequences for its citizens and residents. One of those is the effect of the extended lock-down on travel and tourism, both local and international.

Is it worth the risk of allowing UK tourists into safe countries with well-managed Covid-19 responses?

A tension exists between the appetite from travellers and destination countries’ willingness, or not, to approve such travel. There is no greater example of this tension than the hugely important UK tourist market. The UK continues to be the largest contributor to travel and tourism, for many of the destination markets affected by the Coronavirus pandemic. Hoteliers and tourist companies must balance their natural anxiety for generation of revenue with the risks of allowing visitors from a country that has poorly managed its Covid-19 response. The effect of Johnson’s U-turns, inconsistencies and failings have never been more acutely felt, by either the population or by foreign markets who depend on the British tourist.

“Clusters” of low-infection rate countries have started to emerge as these nations agree, between them, on travel arrangements with fewer restrictions. Examples include Australia, New Zealand and Israel, who have reached an agreement with Austria, the Czech Republic, Denmark and Greece. The ‘Baltic Bubble’ of Latvia, Lithuania and Estonia will allow free travel between these countries, with others required to self-isolate.

However, for the UK it may mean a shut-out. In May, a number of papers including the Metro, Mirror, Daily Star, and even regional papers like Coventry Live have reported a singular message (the message is copied verbatim in most papers so the original source is not clear): “Brits may not be welcome in Europe this summer because of Covid-19 response”. One of Spain’s regional tourism ministers has stated that “Britain had destroyed its chance for holidays with its slow response to the virus” and “taken too long to adopt containment measures”. Some Spanish regions have decided to prioritise the arrival of German and Austrian passengers ahead of Brits. This has involved advance discussions with major German operators such as TUI that have strong presence in both markets.

For a while, it looked as though France would lead the way in barring UK tourists from entering the country, as part of its push to keep all non-EU (the UK is still part of the EU but leaving) traffic at bay. A further proposal saw UK visitors having to undertake a mandatory 14-day quarantine on arrival. Both measures were shelved when the French consulate tweeted that “the UK would not be affected by the quarantine measures”. This decision was not, however, without controversy, as many respondents to the announcement made clear that UK visitors would constitute a clear source of risk. UK tourists would have been in a very different position had the UK government implemented a sensible plan two weeks earlier than it did, and not cancelled its testing programme.

The challenge the UK faces, despite ministers now arguing that international comparisons are not appropriate, is that as the “bad boy” of Europe, it is in an indefensible position. The reality is that with such a high number of deaths, it is simply not able to offer a rebuttal. The reality is that now the fate of British tourists is in the hands of the destination markets, each of which must carefully weigh up whether the risk of allowing tourists from Europe’s worst-managed coronavirus country, is offset by the financial benefit of their entry.

Perhaps a combination of testing on departure, plus testing on arrival and strict isolation rules for any positive results, might be the solution. However, as has been argued by many in the industry, ensuring social distancing rules in airports is impossible and so a positive result without a tracker app will continue to represent significant risk. Those in contact with a potentially infected passenger, disperse quickly on arrival and then interact with members of the local population and other foreign visitors.

At the time of writing, the UK press is reporting that the country’s latest proposal will be to ensure a two-week period of self-isolation for anyone entering the UK, including returning holiday-makers. Apart from a personal aversion to this, because if I travelled it would be the fourth period of self-isolation my family would be experiencing, the solution is yet one more demonstration of how the UK government looks at things the wrong way around.

Surely, with the country topping the charts for infection rates, number of cases and deaths, the tests should be done before people leave the country, not least of which to avoid contagion in airports and planes? What sense is there in a country that is considered among the most infected in the world, and with the poorest management of the virus, sending infected people abroad, to infect other countries, and then testing those who are returning from those safer countries? If the UK government started to focus on getting its own house in order rather than throwing up unnecessary barriers, it might avoid a repeat of the fiasco of its testing “strategy”. In effect, taking responsibility for the measurement of temperature prior to entry into an airport terminal could be successfully combined with Covid-19 testing a few days prior to departure, to ensure results arrive as close as possible to the travel date. In terms of publicity, the government would also have found a way to increase its testing and achieve its now, new, target of 200,000 tests per day. What better way than to use tourism as a way to achieve government testing targets?

Will national tourists, or regional tourists who can drive, kick-start the recovery?

The extent to which national tourists will compensate for the drop in foreign visitors, many of whom cannot travel to their preferred destinations, will change from market to market.

Regions such as mainland Greece should benefit from tourists who are able to drive down from their home countries such as Bulgaria, Romania, Hungary, together with visitors from Baltic states, willing to travel greater distances over a few days. Not only will there be a sense of increased safety by avoiding large groups of people at airports, but also greater independence and the option of choosing more isolated accommodation. Tourism Minister Haris Theocharis echoes this view, saying that “travelling by road will be safer initially than flying.”

In Germany, consideration is being given to allowing tourism flow with neighbouring markets that can access each other by car.

In a country such as Portugal, that only has a border with one neighbour, Spain, this is more limited. Terrestrial transport, much like the flow of rivers, is completely dependent on the Spanish government keeping borders open. Regional tourism, of which Spain represent by far the largest foreign group, is completely outside Portuguese control. In addition, returning Portuguese residents in other EU states, primarily France where the Portuguese community numbers almost 1,000,000, represent a huge source of revenue for the country. It is estimated that the inability of Portuguese nationals, most of whom travel by car via Spain, to return home for summer holidays, will cost the Portuguese economy around €900 million.

Portugal has received high praise from its neighbouring country Spain, including its politicians and the media, as an example of a well-managed Covid-19 response. It is therefore possible that this sort of praise will convince Spanish tourists to visit Portugal ahead of taking a holiday in their home country. Initiatives such as the Safe & Clean described below, can only help. As Spain is the country that represents the largest number of nights of accommodation among all foreign visitors, reigniting Spanish tourism will be crucial for the restart of the economy. This is particularly important for border regions such as the Eastern Algarve, the north of Portugal and several inland towns located close to the border, such as Covilhã which is the gateway to the Serra da Estrela.

National tourism, which represents around a third of total tourism, is unlikely to provide the answer given the effect of the Covid-19 crisis on the disposable income of Portuguese families.

For Portugal, therefore, the restart of its tourism economy will largely depend on foreign tourists and two important markets, one established (the UK) and one emerging (the US), are currently under threat due to their respective poor handling of the Coronavirus pandemic. Despite a fall of over 54%, British tourists led the way in bookings in March, for example.

To lose access to markets such as the UK, whose spends per day are generally above average, due to poor Covid-19 management, would be a pity. But that is the reality that the Southern European market must face.

New hygiene standards: how effective will new initiatives be?

Public opinion of destinations will be influenced by experiences from other tourists. As reports emerge of how safe tourists are and feel, how local businesses and populations have helped in creating a safe environment, and how specific accommodation meets safety criteria, certain markets will stand out from others. It is possible that destination popularity may be affected, to a degree, by this feedback. While Spain will always be a leading tourist destination, for example, a province that manages its social distancing better, while still providing a good tourist experience, will stand out from another and as a result gain new followers and visitors. New beaches, “off the beaten track” in the past, will become more “popular”. Regions considered remote may become the new trend.

While this feedback from the consumer is not available, countries are turning to certification as a way of boosting consumer confidence. Singapore adopted the SG Clean certification. Portugal has implemented a “Clean & Safe” stamp that may be used by tourist establishments and operators that adhere to a set of defined hygiene standards.

As an aside, the use of English in the first version of the certification “stamp” was below par. As a nation, the Portuguese pride themselves on having the best level of English as a second language, of any Southern European nation. For this reason, it is right that Portugal Tourism has quickly produced a new text for the safety badge to more unambiguously communicate the message.

Adherence to the scheme is voluntary and without doubt essential for larger establishments without which consumers will hesitate in making bookings, for example. This is particularly the case if the larger players in the industry such as large resorts, hotels and operators, sign up to self-certification. Any large operator that has not adhered to the scheme will find themselves at a disadvantage.

With adherence to this sort of initiative comes added bureaucracy. Smaller establishments, in particular those involved in local lodging, or Alojamento Local (AL), are unlikely to adhere to the certification for a few reasons:

- Additional inspections of establishments only occur for those that sign up. So, not only does compliant accommodation have to adhere to a new set of rules, but the risk of interruptions, fines and the administrative burden that comes with any such programme in Portugal, will create further costs and worry for small accommodation owners and managers. Much like the situation between registered and (admittedly smaller number of) unregistered homes in the AL market, those that have formally registered have borne the brunt not only of inspections but of higher tax;

- Some requirements are impossible to meet for a smaller property, namely the need for a secure self-isolation location for anyone suspected of infection, complete with self-contained bathroom facilities. In studios, 1- and 2-bedroom properties with a single bathroom, and in properties where no excess capacity exists (for example, a sleeper couch that is not being used) meeting this requirement only risks a fine;

- Management of third-party resources, such as cleaning, is impossible to control fully. Most importantly, it would be a risk to accept responsibility for operations over which owners and managers have little control. Staff involved in the management of short-term rentals are typically seasonal workers who make most of their money in the busy peak season. Mostly working on “recibos verdes” or indeed in the parallel economy, paid in cash, only the most organised and larger cleaning and management companies are able to support keeping their staff as employees on their payroll. In that instance, implementing new training and procedures is feasible. For smaller companies with a seasonal and changing subcontractor base, this is not practical. Most owners will not wish to take on third-party risk.

Ultimately, therefore, in many lodging establishments, the level of cleanliness and hygiene will depend on the quality of the service providers. There is an underlying motivation for those in the sector who must continue to work, as it is the source of their livelihood, despite the risks. The fear of contagion means that not only will workers in the sector self-regulate in their use of protective equipment, but also in terms of methods of cleaning, types and quantities of cleaning products used, and even methods of waste disposal.

Changing behaviours: the new norm?

There is already discussion about whether home-based working will become the new norm. Short of absolute need, for example engagement with a client during a visit, our business has operated this approach for six years. Admittedly the model was developed to allow employees greater freedom and control over their own time management; reduce unnecessary activity such as office chatter, coffee and smoke breaks; eliminate unnecessary travel time; and save costs. Already, I never go into London for one meeting. Unless I can fill an entire morning/afternoon or a full day with necessary meetings or relationship management opportunities, I decline any and all travel to cities with complex or expensive travel, transport and parking issues.

The workforce at large has begun to understand the principle of time optimisation and the benefits of remote working. However, there is additional motivating factor, and that is that many people are fearful of unnecessary contact. They realise that they have no idea of whether another person may introduce risk of contagion and disease into their lives and therefore are reluctant to foster contact except where absolutely necessary. Polls in the UK, for example, show that a majority of people are against the easing of lock-down measures. It will take some time, and some uncomfortable, awkward moments, before a new level of familiarity is established.

The tourism industry will also face changes. In hotels, is this the end of the buffet? Does this mean that all kitchens will face the pressure of customer scrutiny behind glass panels? Do we even trust food whose preparation we cannot see? While restaurants closed and take-aways remained open, do we trust that the food which is delivered is not infected? Has someone in a remote kitchen contaminated it with saliva or sweat, for example? Will all food require a final cooking in the home to ensure the destruction of any contamination via the use of heat?

A Greek hotel is going to implement a process of assigning restaurant and swimming pool seating to guests to avoid cross-contamination. I have seen this already in operation in hotels in Cyprus some years ago. Dinner tables and eating hours will be scheduled (similar to that on cruise ships). The assignment of pool seating such as loungers is an excellent solution, as it will avoid the rush by British and German guests who get up at the crack of dawn to lay a towel down on a lounger and “reserve it”. Southern European guests who typically tend to emerge much later into the sunshine, will be pleased.

In the real estate industry, will hand shaking and kissing disappear? Will larger cars be needed to ensure distancing, or will clients now have to follow in their own vehicle? Will protective equipment such as masks be a requirement for client visits? Will clients be provided with hand gel?

What effect will Covid-19 have on prices of rentals and real estate?

Given lower overall demand, there should be enough property owners who, worried about falling revenue, will offer discounts. Short-term price falls are to be expected, and this trend has already been observed extensively, for example, in rentals in Porto, summer prices in the Algarve, and the number of cheaper short-term rentals making the switch to long-term rents (although this trend will reverse the minute the market recovers).

We have already seen a trend in opportunistic bargain-hunting by foreigners (for example in searching for much cheaper longer lets, or waiting for property prices to fall), but the local population is likely to seek similar discounts through sheer need. Owners and managers need to think seriously about how much discount to offer, if at all. A substantial fall, particularly in rental prices, will undo much of inflationary correction that has occurred in the last 4-5 years. Portugal’s prices had started to match much more fairly its reputation as a quality destination for tourism, retirement and investment. The country and participants in the tourism and related sectors (such as real estate and rental accommodation) must avoid the temptation of reverting to a “bargain basement” mentality. It will take courage to educate potential clients, and there will be a risk of the loss of potential business. For the sustainability of the sector, including the ability to maintain employment and to implement training and safety initiatives, pricing compatible with desired service level must be maintained.

Owners should be encouraged to be flexible about price and conditions but to firm up cancellation policies. Too many tourists are still expecting full Coronavirus refund policy, but owners and managers need to start linking refunds only to government advice or specific travel restrictions, as opposed to any spurious “link” to Covid-19. A rebalancing of rights must occur between tourists and tenants, who thus far have (and rightly so) received most support, and owners and managers, who now need to rebuild their income streams and businesses.

Real estate prices are unlikely to experience significant falls. Knight Frank projects that Lisbon will be one of only four cities globally, together with Monaco, Vienna and Shanghai, that will experience price growth. Large developers, in particular of luxury real estate, have been making bullish comments about the continued price increase and demand. These statements are underpinned by reports that prices of luxury real estate in Lisbon will surpass those of Madrid. Reasons for the robustness of pricing include the relative lack of stock, in particular new-build product. Much like during and after the financial crisis, more than 50% of all real estate development projects have been postponed or stopped, and this adds to pent-up demand.

Because of the financial impact on the local Portuguese population, the real estate sector is one which is likely to be rescued by foreign buyers. The underlying motivations for these buyers will remain unchanged, despite Coronavirus. Some caution and hesitation may occur, but a retiree who has identified Portugal as their destination, will not, in particular due to the good Covid-19 management, change their decision. Part of this motivation is that Portugal represents value for money. Thus the bulk of transactions from important markets such as the UK, will be from buyers looking for reasonably priced real estate in the middle market.

It is therefore a pity that most of the events and conferences that promote moving to or investment in Portugal, many of which partly financed by government grants (read, paid for by the taxpayer), continue to have as their main participants the sellers of expensive real estate in areas such as Quinta do Lago and Vale do Lobo, as well as multi-million projects in Vilamoura or Lisbon or in “new luxury destinations” south of Lisbon. Until Portugal’s tourism and promotion authorities, and the limited circles of associations and bodies that feed into and off this select group, wean themselves off this dependence on luxury, the benefit of Portugal’s intrinsic marketing power will only be harnessed by and remain concentrated in the hands of an elite few. This has the obvious limitation of creating a dependence on the luxury sector for a recovery and a self-fulfilling effect of continuing to concentrate the power in the hands of large players. If some medium-sized players could find the courage and way to counter institutional initiatives with private initiatives aimed at different sectors, the democratisation of the market and its successive multi-level recoveries could begin. Without collaboration, however, the recovery of the mid-market will always lag that of the larger players.

Decisions affecting access by markets such as the UK to the Portuguese market will inevitably have an impact, not only on tourism, but on investment. Retail investment, made by individuals, requires “boots on the ground” and contact with the country. Anything that inhibits or delays this contact, will affect the speed of any recovery. The impact of the UK’s poor Coronavirus strategy will have a knock-on impact on Portugal’s tourism and real estate sector.

An obvious opportunity: can Portugal remarket its low-density areas as the ideal destinations for safe investment?

Portugal’s Golden Visa programme has been, until overtaken recently by Greece, Europe’s most successful residence-by-investment programme. Low population density areas benefit from a discount of 20% relative to normal Golden Visa investment levels. This means, for example, that the usual €500,000, is reduced to €400,000, in order to encourage investment into regions that historically have received less inward investment.

Portugal’s Golden Visa programme has been, until overtaken recently by Greece, Europe’s most successful residence-by-investment programme. Low population density areas benefit from a discount of 20% relative to normal Golden Visa investment levels. This means, for example, that the usual €500,000, is reduced to €400,000, in order to encourage investment into regions that historically have received less inward investment.

Traditionally, these regions have received less attention because they are further from airports, have smaller towns, and less developed infrastructure. But It is likely that the search will increase for accommodation options in regions where social distancing is easier. In particular, nationalities that already have concerns about seeking more isolated locations, may well be attracted to this type of offering. The added benefit is that the real estate in these regions also represent much greater value for money. For example, €400,000 might represent a 2-bedroom apartment in Lisbon and no Golden Visa, while the same investment might purchase a 3-bedroom villa with a pool and a Golden Visa in a low population density area.

In addition to the obvious inland areas and provinces that clearly qualify for reduced investment due to t heir low populations, the astute investor will also seek out the few coastal areas that have this status, but also benefit from greater tourism flows. These regions represent a “safe” tourism investment financially and in terms of personal safety. As it is unlikely that the government will focus any of its attention on this “niche” market, it will be up to the individual investor to educate themselves about these opportunities and to seek them out.

heir low populations, the astute investor will also seek out the few coastal areas that have this status, but also benefit from greater tourism flows. These regions represent a “safe” tourism investment financially and in terms of personal safety. As it is unlikely that the government will focus any of its attention on this “niche” market, it will be up to the individual investor to educate themselves about these opportunities and to seek them out.

Any low density coastal Golden Visa opportunities will be time-limited, as changes to the GV programme, announced at the start of the year, have only been suspended because of the need to focus on Covid-19 and its hugely negative economic impact. Based on past stated intentions, it is likely that at some point in the future coastal locations will be excluded.

A path out of lockdown for the Portuguese tourism industry: what key measures should government be taking?

The moment is ripe for tactical, short and medium-term measures rather than any structural change. Portugal should:

- Continue to emphasise and market its record of safety, including any enhanced measures such as the Safe & Clean initiative for larger establishments and group operators;

- Implement additional measures such as temperature control in large public spaces such as airports, including a link to tracking of arrivals showing any symptoms, and family members, to ensure that controlled flows of passengers can continue;

- Work with other governments to implement pre-departure health checks;

- Place special emphasis on the marketing of Portugal as a destination to select communities in Spain, such as Madrid, western Andalucía and Galicia;

- Immediately support national and international airlines in increasing autumn and winter flights from desirable destinations. TAP’s “spend a day in Lisbon” on layover should be adapted to a “free internal onward flight” initiative. This will get people out of the main Lisbon hub to Porto, Faro and the islands. Even Beja could be considered;

- To better understand and respond to the unique challenges of smaller operators, provide a platform for SME business owners, rather than the same, headline-monopolising large resort or developer owners and managers, to share views and opinions. There should also be a concerted effort by the printed and online press, to allow for more diversified opinion and comment. Large groups with substantial investment are of course very relevant to the greater economy and substantial contributors of tax revenues as well as, in some cases, large employers. However, the monopolising of real estate reporting and opinion in the last few months by managers or administrators of companies with hundreds of millions of investment and focused on the luxury space, is largely irrelevant at the SME level. It offers no comfort to those whose businesses are faced with immediate, short-term cash flow issues;

- Immediately reduce taxation on 6-month plus rentals, using a rule that at least 80% of the occupation must be in the “off-season”, bringing them in line with local lodging tax rates;

- When any changes are made to the Golden Visa programme, retain the same rules for all low-density regions, regardless of whether located inland or the coast;

- Longer term, the simplification and stabilisation of the country’s constantly-changing and mostly increasingly penalising tax and fiscal regime, is of utmost importance. If stable, long-term investment is to be sought from businesses of all sizes, investors must feel they will be treated fairly. Currently real estate related businesses and assets attract a disproportionate amount of complexity and change (and tax). Again, large transactions are often insulated from this issue because, while facing equal bureaucracy, the size of investments mean that financial gains will more than compensate for complexity. This is not the case for smaller players.

[/av_textblock]